At 74, Larry Allison’s alarm still rings at 5.15am two days a week. Instead of settling into a quieter retirement, the former merchant banker and removalist climbs into a school bus in Port Stephens on the NSW north coast, because he says he cannot make the numbers work otherwise.

He says the past year has brought sharp increases across the essentials. “Everything just keeps going up – more than the rate of inflation,” Allison said. “Over the last 12 months, our electricity is up 33 percent, insurance has gone up by 20 percent, and it just doesn’t stop.”

Allison once expected to retire at 65, but now believes he will need to keep working until at least 80. In a Change.org petition, he spelled out what that feels like. “I wake up each week knowing that I still have to work two days just to keep my head above water,” Allison wrote. “I am an age pensioner, and after a lifetime of hard work, it’s disheartening to see that I can’t afford to slow down and enjoy my golden years at home. “Instead, I am forced to continue working because the cost of living has become unbearable.”

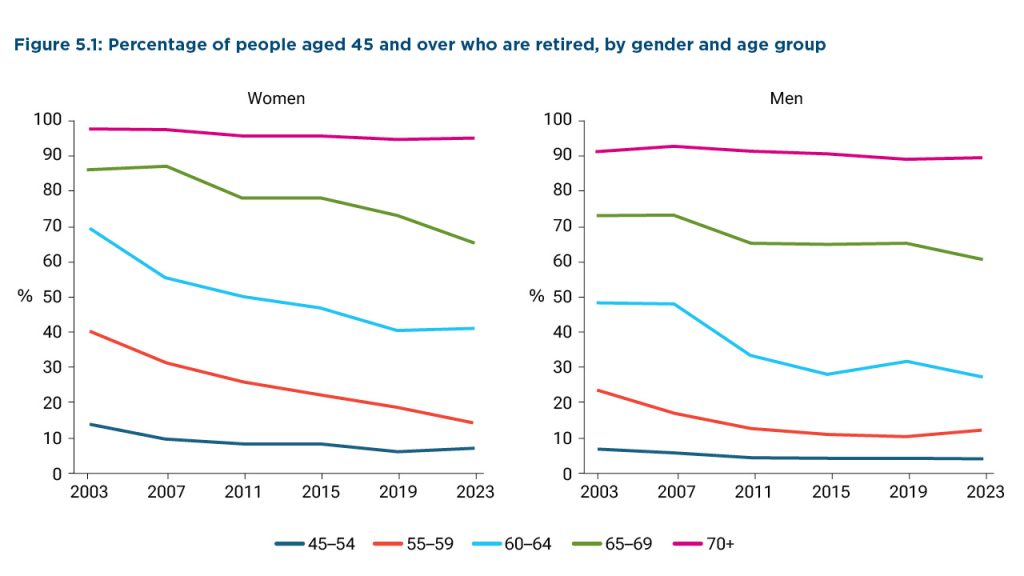

His experience reflects a broader shift, with more Australians delaying full retirement. Data from the Household, Income and Labour Dynamics in Australia (HILDA) survey shows retirement rates for people in their early sixties have fallen sharply over the past two decades. In 2003, about 70 percent of women and close to half of men aged 60 to 64 had fully retired. Today, that has dropped to 41 percent of women and 27 percent of men. Even among 65 to 69-year-olds, full retirement is less common than it once was, with 66 percent of women and 61 percent of men fully retired, down on levels seen twenty years ago.

Working longer can also come with a heavy physical and mental load. To keep his heavy vehicle licence, Allison completes annual driving tests and regular medical checks, including visits with an endocrinologist, a heart specialist and a GP, with a cognitive test to be added this year. “I had open-heart surgery three years ago… but I still managed to get back to work,” he said.

For many older workers, frustration also centres on how paid work affects the Age Pension. Under the income test, once a single pensioner earns more than $218 a fortnight, or $380 for a couple, pension payments are reduced by 50 cents for every extra dollar earned. Allison says that can make additional days of work feel pointless. “When I was working three or four days a week, I was losing 50 cents in every dollar, plus paying 30 cents in tax,” Allison said. “There was no point.”

That argument sits behind National Seniors Australia’s “Let Pensioners Work” campaign, which is pushing for employment income to be fully exempt from the Age Pension income test. The group says the current settings discourage older Australians from taking shifts, even as many industries face staffing shortages.

Billy Pringle, Senior Policy Officer at the Combined Pensioners & Superannuants Association, says the cost-of-living squeeze is hitting pensioners hard, even though the pension is indexed. He argues indexation arrives after price rises have already done the damage. “Pensioners are always having to play catch-up,” Pringle said. “We’ve heard from people who are eating less nutritious meals because they aren’t able to get fresh fruit and vegetables… or they might be skipping meals altogether.”

He says the situation can be even worse for those who cannot keep working. “People have paid tax their whole life with the promise that they can retire, and then they are forced back into the workforce because of circumstance.”

The pension is adjusted twice a year using a “triple-check” indexation method that compares the Consumer Price Index with the Pensioner and Beneficiary Living Cost Index, then benchmarks against Male Total Average Weekly Earnings. But Pringle argues these measures can still fail to reflect real household pressure, especially for renters. He notes that rent has a relatively small weighting in the CPI and a larger one in the PBLCI, yet in practice it can consume far more of a person’s budget. “there’s very few people for whom rent is only six or even 20 percent of their income and of their costs; mostly it’s north of 30 percent.”

Recent changes to the Work Bonus increased how much employment income pensioners can earn before it reduces their payment, including a higher Work Bonus Bank limit. But Allison says the buffer can vanish quickly when major bills land. “We just got our last electricity bill, it was $954 for the last quarter, and we have also just paid our rates – there goes another $2700,” Allison said.