Supermarkets, airlines and power companies are charging ‘exploitative’ prices despite reaping record profits

<p><em><a href="https://theconversation.com/profiles/sanjoy-paul-1141384">Sanjoy Paul</a>, <a href="https://theconversation.com/institutions/university-of-technology-sydney-936">University of Technology Sydney</a></em></p>

<p>Australians have been hit by large rises in grocery, energy, transport, child and aged care prices, only adding to other cost of living pressures.</p>

<p>While extreme weather and supply delays have contributed to the increases, an inquiry into what’s causing the hikes has confirmed what commentators and consumers suspected - many sectors are resorting to dodgy price practices and confusing pricing.</p>

<p>Headed by the former Australian Consumer and Competition Commission (ACCC) boss, Allan Fels, on behalf of the ACTU, the inquiry found inflation, questionable pricing practices, a lack of price transparency and regulations, a lack of market competition, supply chain problems and unrestricted price setting by retailers are to blame for fuelling the increases.</p>

<p>The inquiry, which released its <a href="https://www.actu.org.au/wp-content/uploads/2024/02/InquiryIntoPriceGouging_Report_web9-1.pdf">final report</a> on Wednesday, is one of four examining price rises. The other three are being undertaken by a Senate committee, the Queensland government and the ACCC, which has been given extra powers by the government.</p>

<h2>Prices vs inflation</h2>

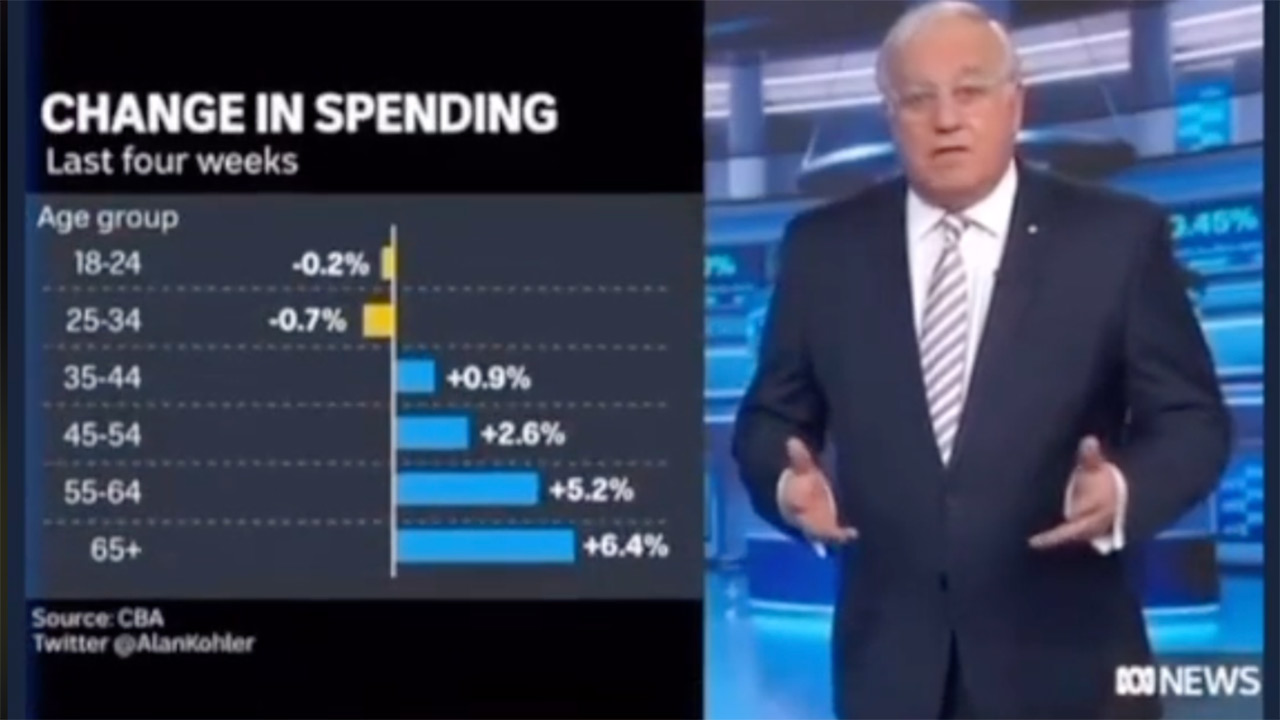

<p>The inflation rate in Australia peaked at <a href="https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/latest-release">7.8%</a> in December 2022 and has been gradually dropping since then.</p>

<p>While the inquiry found higher prices contributed to inflation, it reported that businesses claimed it was inflation that caused price rises - making it a chicken-or-egg kind of problem.</p>

<p>However, many businesses made enormous <a href="https://theconversation.com/amid-allegations-of-price-gouging-its-time-for-big-supermarkets-to-come-clean-on-how-they-price-their-products-219316">profits</a> in 2022-23, which the inquiry said contributed to rising prices and inflation. In most cases, post-pandemic profit margins were much higher than before the pandemic.</p>

<h2>How prices are set</h2>

<p>Business pricing strategies had a big impact on product prices.</p>

<p>In Australia, businesses often provided partial and misleading pricing information which differed from the actual price. For example, supermarkets were “<a href="https://www.afr.com/politics/federal/accc-warns-supermarkets-about-discount-claims-20240114-p5ex1s">discounting</a>” products by raising prices beforehand.</p>

<p>These practices helped raise prices and were “exploitative”, the inquiry found.</p>

<p>A lack of transparent pricing information caused a poor understanding by consumers of how prices were set. This was significantly worsened by a lack of competition. While market concentration was a major issue, the inquiry found prices in Australia are way higher than in many other less competitive markets.</p>

<p>Large price increases occurred across many sectors:</p>

<p><strong>AVIATION</strong></p>

<p>While it is free to set any price for airfares, Australia’s largest and highest profile aviation company, Qantas, has been <a href="https://www.thenewdaily.com.au/life/2023/12/28/qantas-deceptive-conduct-accc">accused</a> of price gouging since the pandemic.</p>

<p>According to the inquiry report, Qantas made a profit of $1.7 billion in 2023 - 208% higher than in 2019. At the same time, its reputation has been badly damaged by unreliable timetables, lost baggage and so-called <a href="https://www.9news.com.au/national/qantas-files-legal-defence-refutes-accc-case-and-ghost-flight-claims/9a6296c9-9238-4053-9f36-cc3cbf1f8a55">“ghost” flights</a> (selling tickets for a flight that’s been cancelled or doesn’t exist).</p>

<p>Despite its huge profits and poorer service, Qantas passed on extra expenses to consumers in the form of higher airfares, the inquiry found.</p>

<p><strong>BANKING</strong></p>

<p>The banking industry has a long history of being tardy in passing on the Reserve Bank’s cash rate cuts to consumers. However, when the reserve raised the cash rates, banks immediately increased their standard variable rates and passed them on to customers. This practice keeps the bank’s profit margin higher.</p>

<p>According to the inquiry report, the major banks’ average profit margins have been higher since May 2022 than in the 15 years before the pandemic. For 2022-23, the four big Australian banks’ profit margins were 35.5%, compared to an average of 32.4% from 2005 to 2020.</p>

<p><strong>CHILDCARE</strong></p>

<p>Australian households spent a good portion of their income on childcare, and for many of them, it was <a href="https://www.vu.edu.au/sites/default/files/mitchell-institute-assessing-childcare-affordability-in-Australia.pdf">unaffordable</a>.</p>

<p>In Australia, the lack of availability and difficulty in switching services makes it even harder for working parents to find alternative options. This indicates parents are forced to pay more if the service providers raise prices.</p>

<p>The inquiry found the childcare sector increased fees by 20% to 32% from 2018 to 2022. Accordingly, Australian households’ out-of-pocket expenses for childcare increased more than the rate of wage growth. For-profit childcare businesses have higher margins than not-for-profit centres.</p>

<p><strong>ELECTRICITY</strong></p>

<p>In recent years, electricity price increases have impacted all Australian households. The inquiry found both wholesale and retail electricity pricing strategies were responsible for these increased prices.</p>

<p>It reported that wholesale price increases were mainly responsible for an estimated 9% to 20% increase in electricity bills in 2022-23.</p>

<p>The report noted the “price bidding system” was largely responsible for increasing wholesale electricity prices.</p>

<p>The inquiry was critical of the profit margin of AGL, a leading electricity retailer:</p>

<blockquote>

<p>It would seem that AGL needs to explain why consumers are paying $60.10/MWh more than seems to be justified by cost differentials. That is, for every consumer bill of $1,000 there is an apparent excess to be explained of $205.61 relative to prices charged to large business customers and not accounted for by genuine cost differences.</p>

</blockquote>

<p><strong>SUPERMARKETS</strong></p>

<p>Supermarket prices have received the most attention recently with the main providers being accused of price gouging.</p>

<p>As has occurred in other sectors, profit margins were well above pre-COVID levels. In 2023, the margin was more than 3.5% compared to less than 3% in 2017 and 2018.</p>

<p>In Australia, <a href="https://www.smh.com.au/politics/federal/not-happy-little-vegemites-food-prices-rising-faster-than-inflation-20230522-p5da9w.html">food prices</a> also increased well above the inflation rate.</p>

<p>According to the inquiry, the price increases for groceries between March 2021 and September 2023 varied between 19.2% and 27.3% for different categories, including cheese, bread, milk, eggs, dairy products and breakfast cereals.</p>

<p>Farmers recently <a href="https://www.news.com.au/finance/business/retail/aussie-farmer-shipping-beautiful-melons-to-japan-rather-than-deal-with-coles-and-woolworths/news-story/bd685cd91f934f31c02c764097f496ae">accused</a> supermarkets of making too much profit from their crops.</p>

<p>This was backed by the inquiry, which found the disproportionate market power held by supermarkets and food processors was of significant concern.</p>

<p>The report noted that supermarkets increased prices when there was a shortage or cost increase, but the opposite did not happen easily when supplies were plentiful and prices were cheaper.</p>

<h2>Issues common to all sectors</h2>

<p>Among the issues common to all sectors were weak competition, a lack of price transparency, the difficulty consumers face switching between suppliers and providers, a lack of pricing policies and a lack of consumer awareness.</p>

<p>While the price rises imposed by service providers and retailers were <a href="https://www.accc.gov.au/business/pricing/setting-prices-whats-allowed">not unlawful</a>, the increases in all sectors were significant and were hurting everyday Australians.</p>

<h2>Fels’ recommendations</h2>

<p>Many of the recommendations were sector-specific, but the one that applied to all areas related to the lack of regulation and pricing policies.</p>

<p>The ACCC should be empowered to investigate, monitor and regulate prices for the child and aged care, banking, grocery and food sectors, the inquiry found. This was necessary to ensure businesses used fair and transparent pricing.</p>

<p>A review of all existing policies was also recommended. For example, the government should use the current aviation review to remove international and domestic restrictions on competition. It was important aviation stakeholders, such as airlines and airports, were involved in the process.</p>

<p>The report suggested the grocery <a href="https://www.accc.gov.au/business/industry-codes/food-and-grocery-code-of-conduct">code of conduct</a> should be mandatory for the food and grocery sector, and a price register for farmers should be created. This should be a government priority to protect farmers from unfair pricing by major supermarkets and food processors.</p>

<h2>Change is needed</h2>

<p>The current pricing practices for all business sectors must improve for greater transparency and to protect Australian consumers from unfair pricing.</p>

<p>The inquiry report’s findings and recommendations are helpful in ensuring fair and transparent pricing policies and improving the current regulations for price settings.</p>

<p>Implementing the recommendations will improve fair and transparent pricing practices and may help Australians get relief from the cost of living pressure in future.<!-- Below is The Conversation's page counter tag. Please DO NOT REMOVE. --><img style="border: none !important; box-shadow: none !important; margin: 0 !important; max-height: 1px !important; max-width: 1px !important; min-height: 1px !important; min-width: 1px !important; opacity: 0 !important; outline: none !important; padding: 0 !important;" src="https://counter.theconversation.com/content/222755/count.gif?distributor=republish-lightbox-basic" alt="The Conversation" width="1" height="1" /><!-- End of code. If you don't see any code above, please get new code from the Advanced tab after you click the republish button. The page counter does not collect any personal data. More info: https://theconversation.com/republishing-guidelines --></p>

<p><a href="https://theconversation.com/profiles/sanjoy-paul-1141384"><em>Sanjoy Paul</em></a><em>, Associate Professor, UTS Business School, <a href="https://theconversation.com/institutions/university-of-technology-sydney-936">University of Technology Sydney</a></em></p>

<p><em>Image credits: Getty Images </em></p>

<p><em>This article is republished from <a href="https://theconversation.com">The Conversation</a> under a Creative Commons license. Read the <a href="https://theconversation.com/supermarkets-airlines-and-power-companies-are-charging-exploitative-prices-despite-reaping-record-profits-222755">original article</a>.</em></p>